Well, the easy part is done – that is refuting the talking points of the FHLBs argument to maintain the status quo.

Next up, coming up with the right balance of a sustainable business model for the FHLBs and supporting the housing initiatives commensurate with the acute need for housing solutions and the FHLBs professed desire to contribute.

2023 results are probably not the right baseline as last year the FHLBs generated record profits almost double any previous year. Driven by the combination of high advance lending to members, high short term interest rates and very attractive cost of raising new debt, 2023 may or may not be repeatable (though 2024 is off to a similar trajectory).

What is required is a thorough review of the conditions that influence FHLB performance so that a more enduring perspective of how much the FHLBs can invest in affordable housing initiatives is developed.

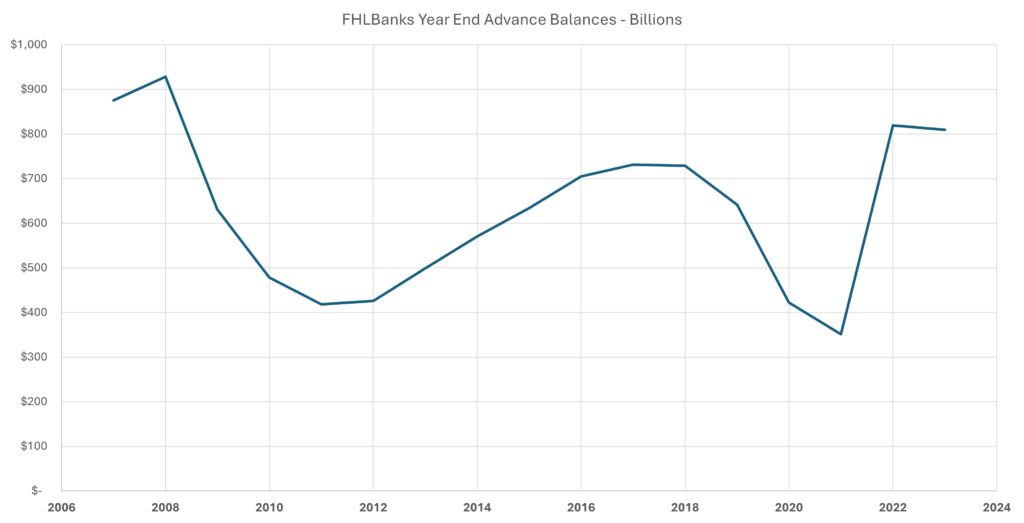

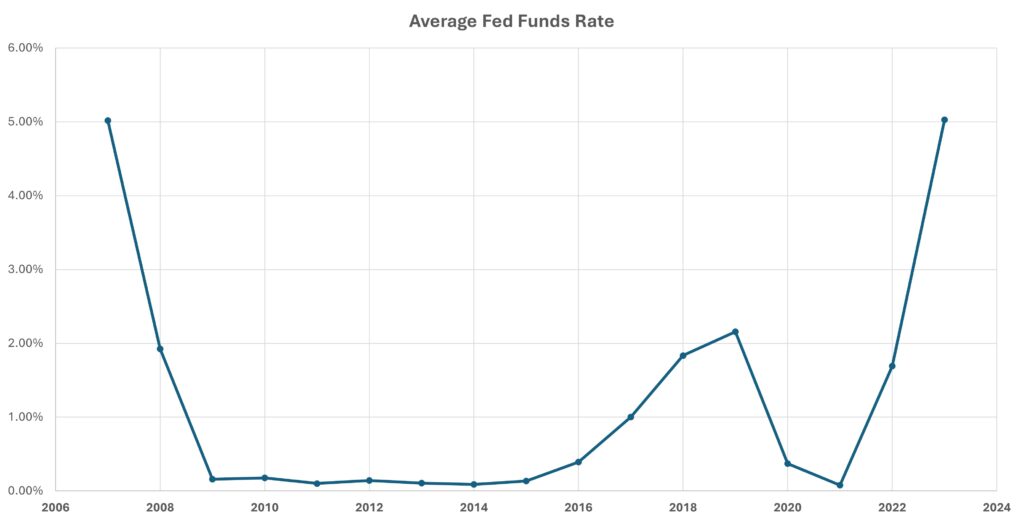

This process is introduced below with two charts, showing the variability of advance loans to members over time, and similarly the volatility of short-term interest rates – both of which influence FHLB profitability. Analysis of the interaction of these and other variables will begin next week.

Other historical perspectives are available in the Tables and Charts tab above.

Lastly, the FHFA, the regulator of the FHLBs, has issued a request for input – https://www.fhfa.gov/news/news-release/fhfa-requests-input-on-fhlbank-system-mission on the mission of the FHLBs, ways to measure mission achievement and ways to encourage members to connect to the mission. It asks the right questions.

One Response

Absolutely the Federal Home Loan Banks can invest more — in grants and long-term discount loans – for housing and community development.

Ten – 20, 30, 50 – precent of net profits is probably not the right approach since the FHLBanks regularly act to lower their profits by paying their Presidents $2-$4.3 million a year and their staff extremely well while also just lowering advance rates to their borrowing member institutions.

Interested to hear options to better set an investment standard that the FHLBanks can’t game.